Reference Manual on Scientific Evidence: Fourth Edition (2025)

Chapter: Reference Guide on Estimation of Economic Damages

Reference Guide on Estimation of Economic Damages

MARK A. ALLEN, CARLOS BRAIN, AND FILIPE LACERDA

Mark A. Allen, J.D., is Principal at Cornerstone Research.

Carlos Brain, M.B.A., Sc.M., is Vice President at Cornerstone Research.

Filipe Lacerda, Ph.D., M.B.A., Finance, is Vice President at Cornerstone Research.

The views expressed herein are solely those of the authors, who are responsible for the content, and do not necessarily represent the views of Cornerstone Research.

CONTENTS

Damages Experts’ Qualifications

The Standard General Approach to Quantification of Economic Damages

Isolating the Effect of the Harmful Act

General Categories of Damages Measures

Basic Issues Arising in Damages Estimation

Valuation Issues in the Analysis of Economic Damages

Issues Arising in Connection with the Use of the Market Price of the Product or Asset at Issue

Adjusting the market price of ostensibly similar products or assets

Issues Arising in Connection with the Use of Models to Simulate the But-For Price

Realistic modeling of preferences, incentives, and constraints of buyers and sellers

Modeling the impact of the alleged misconduct on demand and supply

Accounting for Market Frictions

Issues Arising in Connection with the Use of Repair or Abatement Costs

Estimating the Period-by-Period Direct Impact of the Alleged Harmful Act

Disputes about whether all economic consequences of the alleged harmful act are being accounted for

Disputes about the use of expected outcomes to estimate the impact of the alleged harmful act

Disputes about the economic situation in future periods

Disputes about the consideration of non-cash effects of the alleged harmful act

Valuing the Period-by-Period Impact of the Alleged Harmful Act as of a Single Valuation Date

Estimating the time value of money

Disagreements about what valuation date to use

Other Issues Arising in General in Damages Measurement

Criteria for Determining the Validity of Data

Quantitative Methods for Validation

Damages with Multiple Challenged Acts: Disaggregation

Disputes About Whether the Plaintiff Is Entitled to All the Damages

The Effect of a Liquidated Damages Clause

Damages of Individual Class Members

Damages as a Basis to Evaluate the Fairness of a Proposed Settlement

Damages Issues in Selected Types of Cases

Estimation of Economic Damages in Consumer Product Liability and Misrepresentation Cases

Defining the Plaintiff’s Economic Position in the Actual and But-For Worlds

Conjoint Analysis and Supply-Side Considerations

Estimation of Economic Damages in Securities Cases

Key Areas of Disagreement in the Economic Analysis of Inflation and Losses Caused

Analysis of “confounding” information

Measuring inflation at the time of purchase

Estimation of Economic Damages in Antitrust Cases

Quantifying Damages in an Antitrust Matter

Before-and-after model of overcharge damages

Difference-in-differences model of overcharge damages

Estimation of Economic Damages from Loss of Personal Income

Estimation of Losses Over a Person’s Lifetime

Calculation of Fringe Benefits

FIGURE

TABLE

Introduction

This reference guide identifies areas of dispute that arise when economic losses are at issue in legal proceedings. We focus on explaining the issues in these disputes rather than taking positions on their proper resolution. We discuss the application of economic analysis within established legal frameworks for damages, cover topics in economics that arise in measuring damages, and, where useful, provide citations to cases that illustrate the principles and techniques discussed in the text.

We begin with a brief discussion of qualifications for damages experts. We then set forth the standard general approach to quantification of economic damages, with particular focus on translating the legal theory of the harmful event into an analysis of the economic impact of that event and choosing the measure of economic damages. Next, we consider disputes that may arise between the parties regarding damages estimation. Such disputes may concern basic issues (e.g., proper damages measure and losses caused), valuation issues (e.g., damages arising on single or multiple dates, and the use of market or other data to estimate damages), other issues (e.g., data validity, prejudgment interest, disaggregation), and limitations on damages. We also discuss damages in class actions as well as the application of damages principles to specific types of cases.

We use brief examples to illustrate the disputes that can arise and provide intuition for relevant economic issues. These examples are not full case descriptions; they are deliberately stylized, attempting to capture the types of disagreements about damages that arise in practical experience, although they are purely hypothetical. In many examples, the dispute involves factual and economic as well as legal issues. We do not try to resolve the disputes in these examples; hopefully the examples will help clarify the legal and factual disputes that need to be resolved before or at trial.

Damages Experts’ Qualifications

Experts who quantify damages come from a variety of backgrounds. The expert should be trained and experienced in quantitative analysis. For economists, the common qualification is a Ph.D. degree. Damages experts with business or accounting backgrounds often have M.B.A. or other advanced degrees, or C.P.A. credentials. Both the method of damages estimation used and the substance of the damages claim dictate the specific areas of specialization the expert should have. In some cases, participation in original research and authorship of professional publications may add to the qualifications of an expert. However, relevant research and publications are not likely to be on the topic of damages measurement per se, but rather on topics and methods encountered in damages analysis.

Professional training and experience in areas relevant to the substance of the damages claim may be required. For example, in antitrust, a background in industrial organization (i.e., competition economics) may be helpful; in securities damages, a background in finance may assist the expert; and in the case of lost earnings, an expert may benefit from training in labor economics.

An analysis by even the most qualified expert may face a motion to exclude under Federal Rule of Evidence 702 as interpreted by the Daubert line of cases.1 Under Rule 702, an expert witness who is “qualified . . . by knowledge, skill, experience, training, or education,” is allowed to testify when

(a) the expert’s scientific, technical, or other specialized knowledge will help the trier of fact to understand the evidence or to determine a fact in issue; (b) the testimony is based on sufficient facts or data; (c) the testimony is the product of reliable principles and methods; and (d) the expert has reliably applied the principles and methods to the facts of the case.

These criteria, which are intended to exclude testimony that is irrelevant or is based on untested and unreliable theories, are often applied to damages analyses. Examples include the following:

- A proposed damages expert may be qualified generally to opine on damages issues but may lack the qualifications necessary to offer an opinion in the context of the particular matter at hand. For example, a labor economist may lack the proper education, training, and experience to opine on damages in a securities matter.

- A proposed expert may have used a methodology that is incorrect as a matter of economics; the results may have been based on insufficient data (e.g., too few observations); or a theoretically sound analysis may not have been properly applied, even if large amounts of data were used in the analysis.

- All or part of a damages analysis may no longer be relevant if certain legal claims have been dismissed, or expert opinion on damages simply may not be needed at all, such as where damages may be determined using a simple mathematical formula.

Even if a motion to exclude fails, it can be an effective way for a party to probe an opposing expert’s damages analysis prior to trial. For this reason, among others, motions to exclude proposed expert damages testimony have become relatively commonplace.

1. Daubert v. Merrell Dow Pharms., Inc., 509 U.S. 579 (1993); Kumho Tire Co. v. Carmichael, 526 U.S. 137 (1999). For a discussion of emerging standards of scientific evidence, see Liesa L. Richter & Daniel J. Capra, The Admissibility of Expert Testimony, in this manual.

The Standard General Approach to Quantification of Economic Damages

In this section, we review the general principles of the standard approach to the estimation of economic damages and basic issues that arise in such estimation. For each principle, there are several areas of potential dispute. The sequence of issues discussed here is intended to identify most of the areas of disagreement between the damages analyses of opposing parties with respect to these principles.

General Principles

We begin by setting forth the standard general approach to damages quantification, with particular focus on defining the harmful event and the alternative, or but-for, scenario. In most cases, the goal of measurement of economic damages is to estimate the plaintiff’s loss of economic value caused by the defendant’s harmful act. The loss of value may arise from a single event, such as overpayment for a consumer product, or it may take the form of a reduced stream of profits or earnings over time. The losses are net of any costs avoided because of the harmful act.

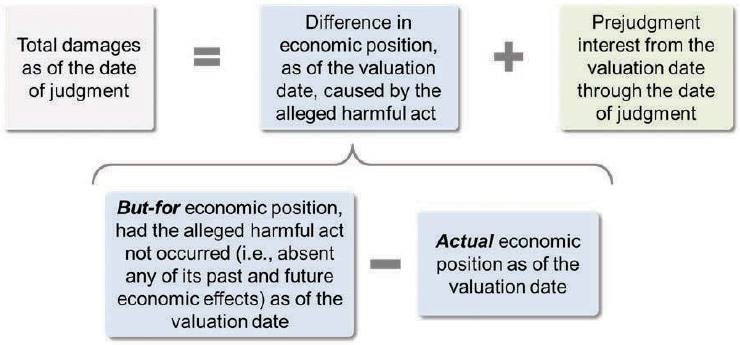

In principle, then, economic damages are the difference between (1) the plaintiff’s economic position assuming that the alleged harmful act had not occurred, and (2) the plaintiff’s actual economic position as a result of the harmful act.2 The former considers the plaintiff’s economic position absent any past and future effects of the harmful act. We refer to this as the plaintiff’s but-for economic position in the but-for world. The latter considers the plaintiff’s actual economic position given the occurrence of the harmful act. We refer to this as the plaintiff’s actual economic position in the actual world.

Figure 1 illustrates the structure of the standard damages study. We begin by estimating the plaintiff’s losses as of the appropriate valuation date. The appropriate valuation date may vary depending on the nature of the loss and the plaintiff’s theory of recovery (e.g., breach of contract, tort, fraud, etc.). Losses are the difference between the plaintiff’s but-for economic position and the plaintiff’s actual economic position as of the valuation date. Note that the plaintiff’s but-for economic position may require estimating past losses as well as future losses, again

2. Damages are sometimes measured based on the defendant’s gain rather than the plaintiff’s losses. If measured based on the defendant’s gain, economic damages are the difference between (1) the defendant’s actual economic position as a result of the harmful act, and (2) the defendant’s economic position assuming that the alleged harmful act had not occurred.

determining their value as of the valuation date. The plaintiff may be entitled to prejudgment interest through the judgment date on their damages as of the valuation date.3

Isolating the Effect of the Harmful Act

The first step in a damages study is the translation of the legal theory of the harmful event into an analysis of the economic impact of that event. As noted above, in most cases, the analysis considers the difference between what the plaintiff’s economic position would have been if the harmful event had not occurred and the plaintiff’s actual economic position as of the valuation date.

The characterization of the harmful event begins with a clear statement of what occurred in the actual world. This characterization also will include a description of the but-for world, including the defendant’s proper actions in place of their unlawful actions and a statement about the economic situation of all relevant parties absent the wrongdoing, with the defendant’s proper actions replacing the unlawful ones. Damages measurement then determines the plaintiff’s hypothetical economic position in the but-for world. Economic damages are the difference between that value and the actual value that the plaintiff achieved.

3. The plaintiff may also be due postjudgment interest, which is interest on the damages award from the date of judgment to the date the defendant satisfies the judgment.

Because the but-for world differs from what actually happened only with respect to the harmful act and its reasonably foreseeable economic consequences, damages measured in this way isolate the change in the plaintiff’s economic position caused by the harmful act and exclude any change in the plaintiff’s economic position arising from other causes.4 Thus, a proper construction of the but-for world and measurement of the plaintiff’s economic position in the but-for world by definition include in damages only the loss caused by the harmful act.

Properly translating the legal theory of the harmful act into an analysis of the economic impact of that event is a fundamental step in the estimation of economic damages. Failure to do so may result in the damages analysis being discounted or excluded altogether. For example, in Comcast Corp. v. Behrend, the U.S. Supreme Court found that the plaintiffs’ expert had put forth a damages model that “failed to measure damages resulting from the particular antitrust injury on which . . . liability in this action is premised.”5 Citing the discussion in the prior edition of this reference guide, the Court determined that the expert’s “methodology . . . identifies damages that are not the result of the wrong” and measures damages “caused by factors unrelated to an accepted theory of . . . harm.”6

4. Reasonable foreseeability is a legal doctrine that courts use to determine whether the consequences of a legal or contractual breach are too remote to be borne by the defendant. Reasonable foreseeability is not a measure of damages, but rather an upper limit on damages. The use of “reasonable” here relates to the legal concept of the “reasonable person” or “economic person,” and concerns actions that a reasonable person or economically rational actor under similar circumstances would take. See, e.g., Richard A. Posner, Economic Analysis of Law (2d ed. 1977); Steven Shavell, Foundations of Economic Analysis of Law (2004); Israel Gilead & Michael D. Green, Positive Externalities and the Economics of Proximate Cause, 74 Wash. & Lee L. Rev. 1517 (2017); John Fabian Witt & Morgan Savige, Foreseeability Conventions, 44 Cardozo L. Rev. 1075 (2023); Russ VerSteeg, Perspectives on Forseeability in the Law of Contracts and Torts: The Relationship Between “Intervening Causes” and “Impossibility,” 2011 Mich. St. L. Rev. 1497 (2011). Reasonable foreseeability is not a term of art in the field of economics. While determinations regarding reasonable foreseeability may impact the damages analysis, application of the concept is not within the purview of the damages expert. As such, the damages expert may require assumptions from counsel as to whether a particular outcome is a reasonably foreseeable consequence of the alleged harmful act.

5. Comcast Corp. v. Behrend, 569 U.S. 27, 46 (2013).

6. Id. at 38 (“‘The first step in a damages study is the translation of the legal theory of the harmful event into an analysis of the economic impact of that event.’ The district court and the court of appeals ignored that first step entirely” (citations omitted)). See also In re POM Wonderful LLC, No. ML 10–02199 DDP RZX, 2014 WL 1225184, at *5 (C.D. Cal. March 24, 2014) (damages expert “made no attempt, let alone an attempt based upon sound methodology, to explain how Defendant’s alleged misrepresentations caused any amount of damages”); In re Domestic Drywall Antitrust Litig., No. 13-MD-2437, 2017 WL 3700999, at *14 (E.D. Pa. Aug. 24, 2017) (expert’s damages model was “riddled with assumptions that divorce the model from the facts”).

General Categories of Damages Measures

In most cases, damages are measured based on one or more of the following six categories: (1) expectation, (2) reliance, (3) restitution, (4) statutory, (5) liquidated, and (6) punitive.7 We discuss each of these in turn.

- Expectation: Plaintiff restored to the same financial position as if the defendant had performed as promised.

Expectation damages typically apply to breach-of-contract claims, where the wrongdoing is the failure to perform as promised and the but-for scenario hypothesizes the absence of that wrongdoing—that is, proper performance by the defendant. Expectation damages are an amount sufficient to place the plaintiff in the same economic position as if the defendant had fulfilled the promise or bargain.8

- Reliance: Plaintiff restored to the same position as if the relationship with the defendant or the defendant’s misrepresentation (and resulting harm) had not existed in the first place.

Reliance damages generally apply to torts and to some breach-of-contract claims. Such damages restore the plaintiff to the same financial position they would have enjoyed absent the defendant’s conduct.9 Reliance most often includes out-of-pocket costs,10 but may also include compensation for lost opportunities when appropriate.11 In such cases, reliance damages may approach expectation

7. The law imposes several limitations on damages, which are discussed below in the section titled “Limitations on Damages.”

8. See John R. Trentacosta, Damages in Breach of Contract Cases, 76 Mich. Bus. J. 1068, 1068 (1997) (describing expectation damages as damages that place the injured party in the same position as if the breaching party completely performed the contract); Spring Creek Expl. & Prod. v. Hess Bakken Inv., 887 F.3d 1003, 1026 (10th Cir. 2018) (defining expectation damages as the amount of damages necessary to place the injured party in the same position it would have occupied had the breach not occurred). See also Restatement (Second) of Contracts § 344(a) (1981).

9. See E. Allan Farnsworth, Legal Remedies for Breach of Contract, 70 Colum. L. Rev. 1145, 1148 (1979) (the objective of reliance damages is to put the promisee, or nonbreaching party, back into the position it would have been had the promise not been made). See also Restatement (Second) of Contracts § 344(b) (1981). Reliance damages include expenditures made in preparation for performance and performance itself. Restatement (Second) of Contracts § 349 (1981).

10. Out-of-pocket costs are expenses incurred by a party in preparing to perform (or in performing) a contract in reliance on the terms of the agreement. This is distinct from the notion of out-of-pocket damages used in securities fraud damages, which relates to the difference between price paid and a but-for price that would have been paid. See the discussion in the section titled “Estimation of Economic Damages in Securities Cases” below.

11. Compensation for lost opportunities embodies the economic concept of opportunity cost, which expresses the relationship between scarcity and choice. Given an economic actor facing a

damages.12 For a tort, the goal of reliance damages is to place the plaintiff in a position economically equivalent to their position absent the harmful act.13 For a breach of contract, measuring damages as the amount of compensation needed to return the plaintiff to the position they would have been in had the contract had not been made in the first place will result in refunding the part of the plaintiff’s reliance investment that cannot be recovered in other ways. Thus, reliance damages may be appropriate where the plaintiff made an investment relying on the defendant’s performance.

Example: Agent contracts with Owner for Agent to sell Owner’s farm. The asking price is $1,000,000, and the agreed fee is 6%. Agent incurs costs of $1,000 in listing the property. A potential buyer offers the asking price, but Owner withdraws the listing. Agent calculates (expectation) damages as $60,000, the agreed fee for selling the property. Owner calculates (reliance) damages as $1,000, the amount that Agent spent to advertise the property.

- Restitution: Plaintiff compensated by the amount of the defendant’s gain from the unlawful conduct, also called compensation for unjust enrichment, disgorgement of ill-gotten gains, or compensation for unbar-gained-for benefits.

Restitution damages are awarded to prevent the defendant’s unjust enrichment from the unlawful conduct. The goal of restitution damages is to restore the defendant to the economic position they would have been in had they not engaged in the wrongful act, and typically includes disgorgement of defendant’s

choice between mutually exclusive alternatives, the opportunity cost of the alternative selected (e.g., entering into a contract with vendor A) is the value of the best alternative not chosen (e.g., entering into a contract with vendor B, C, or D). See, e.g., N. Gregory Mankiw, Principles of Microeconomics 6 (8th ed. 2016) (“The opportunity cost of an item is what you give up to get that item.” (emphasis omitted)).

12. In some situations, reliance damages can exceed expectation damages, but the court may limit damages to the expectation measure. See, e.g., Fairholme Funds, Inc. v. Fed. Hous. Fin. Agency, No. 1:13-cv-1053-RCL, 2022 WL 11110584, at *4 (D.D.C. Oct. 19, 2022) (Plaintiff claimed reliance damages “many multiples higher” than the allowed measure of expectation damages. The court stated, “In contract cases, expectation damages are preferred, with reliance damages considered as an alternative or proxy if expectation damages are not readily ascertainable. . . . [P]laintiffs . . . cannot recover reliance damages so far in excess of ascertainable expectation damages that they would necessarily place those plaintiffs in a better position than they would have been in had the contract been performed.”).

13. See, e.g., East River Steamship Corp. v. Transamerica Delaval Inc., 476 U.S. 858, 873 n.9 (1986) (“tort damages generally compensate the plaintiff for loss and return him to the position he occupied before the injury”).

ill-gotten gains.14 In practice, restitution is often the same, from the perspective of quantification, as reliance damages. If the only loss to the plaintiff from the defendant’s harmful act arises from an expenditure that the plaintiff made that cannot otherwise be recovered, the plaintiff receives compensation equal to the amount of that expenditure.15

- Statutory: Plaintiff’s compensation is an amount established by statute, either as a set amount per occurrence of wrongdoing or determined using a statutory formula. For example, this measure of damages is often found in cases involving violations of state labor codes and in copyright infringement.

- Liquidated: Plaintiff compensated by an amount specified in a legal agreement or contract between the parties.

- Punitive: Compensation to reward the plaintiff for detecting and prosecuting the wrongdoing or to deter similar wrongdoing in the future.

A plaintiff cannot normally seek punitive damages in a claim for breach of contract but may seek them in addition to compensatory damages in connection with a tort claim.16 Although punitive damages are rarely the subject of expert testimony, economists have advanced the concept that punitive damages compensate a plaintiff who brings a case for a wrongdoing that is hard to detect or hard to prosecute.17

Basic Issues Arising in Damages Estimation

Losses Caused

The analysis of losses caused is typically a key part of the analysis of damages. Analyzing damages requires isolating the portion, if any, of the plaintiff’s losses that can be attributed to the harmful act from the portion that can be attributed to other factors.

14. Note the distinction between restitution and reliance damages. The objective of restitution damages is to put the promisor, or breaching party, back in the position in which it would have been had the promise not been made. In contrast, reliance damages seek to put the promisee, or nonbreaching party, back in the position in which it would have been if the promise had not been made. See E. Allan Farnsworth, Legal Remedies for Breach of Contract, 70 Colum. L. Rev. 1145, 1148 (1979). Both measures seek to restore the status quo ante. See also Restatement (Third) of Restitution and Unjust Enrichment (2011).

15. See Restatement (Second) of Contracts § 344(c) (1981).

16. Compensatory damages are damages “sufficient in amount to indemnify [or compensate] the injured person for the loss suffered.” Damages, Black’s Law Dictionary (11th ed. 2019).

17. See Steven Shavell, Foundations of Economic Analysis of Law 244 (2004).

Example: Worker who smokes is the victim of a disease caused either by exposure to xerxium or by smoking. Worker makes leather jackets tanned with xerxium. The disease precludes Worker from earning wages. Worker sues the producer of the xerxium, Xerxium Mine, and calculates damages as all lost wages. Defendant Xerxium Mine, in contrast, attributes most of the losses to smoking and calculates damages as only a fraction of lost wages.

Frequently, the defendant will calculate damages on the premise that the harmful act had no causal relationship to the plaintiff’s losses—that is, the plaintiff’s losses would have occurred irrespective of the harmful act. The defendant’s but-for scenario will thus describe a situation in which the losses happen anyway. This is equivalent to arguing that the harmful act occurred but the plaintiff suffered no incremental losses from it.

Example: Contractors conspired to rig bids in a construction deal. State seeks damages for subsequent higher prices. Contractors’ damages estimate is zero because they assert that the only effect of the bid rigging was to determine the winner of the contract and that prices were not affected.

In other situations, unexpected events occurring after the harmful event (known as subsequent unexpected events) can increase or decrease the plaintiff’s actual loss relative to what might have been expected at the time of the harmful event.

Example: Housepainter uses faulty paint, which begins to peel a month after the paint job. Owner measures damages as the cost of repainting. Painter disputes this measure on the ground that a hurricane that occurred three months after the paint job would have ruined a proper paint job anyway.

A plaintiff may argue that a harmful act has caused significant losses for many years. The defendant may respond that most of the losses that occurred from the injury are the result of causes other than the harmful act. Thus, the defendant may argue that the injury was caused by multiple factors, only one of which was the result of the harmful act, or that the plaintiff’s injury was caused by subsequent events.

Example: Real Estate Agent is wrongfully denied affiliation with Broker. Agent’s damages study projects past earnings into the future at the rate of growth of the previous three years. Broker’s study projects that earnings would have declined even without the breach because of a downturn in the real estate market.

Comment: The difference between a damages study based on extrapolation from the past, here used by Agent, and a study based on actual data after the harmful act, here used by Broker, is one of the most common sources of disagreement in damages. This is a factual dispute that hinges on Broker demonstrating that there is a relationship between real estate market conditions and the earnings of agents. The example also illustrates how subsequent unexpected events can affect damages calculations.

Hypothesizing Legitimate Conduct of the Defendant in Analyzing the Plaintiff’s Economic Position But For the Harmful Event

One party’s damages analysis may hypothesize the absence of any act of the defendant that influenced the plaintiff, whereas the other party’s damages analysis may hypothesize an alternative, legal act. This type of disagreement is particularly common in antitrust and intellectual property disputes. Although disagreement over the alternative scenario in a damages study is generally a legal question, opposing experts may have been given different legal guidance and therefore made different economic assumptions, resulting in major differences in their damages estimates.

Example: Defendant Copier Service’s long-term contracts with customers are found to be unlawful because they create a barrier to entry that maintains Copier Service’s monopoly power. Plaintiff Rival’s damages study hypothesizes no contracts between Copier Service and its customers, so Rival would face no contractual barrier to bidding those customers away from Copier Service. Copier Service’s damages study assumes medium-term contracts with its customers and argues that these would not have been found to be unlawful. Under Copier Service’s assumption, Rival would have been much less successful in bidding away Copier Service’s customers, and damages are correspondingly lower.

Comment: Assessment of damages will depend greatly on the substantive law governing the injury. The proper characterization of Copier Service’s alternative conduct usually is an economic issue. However, the expert must also have legal guidance as to the proper legal framework for damages. Counsel for the plaintiff may instruct the plaintiff’s damages expert to use a legal framework different from that used by counsel for the defendant.

Considering All the Differences in the Plaintiff’s Situation in the But-For Scenario Versus Assuming That Many Aspects Would Be the Same as in Actuality

The analysis of some types of harmful events requires consideration of effects that involve changes in the economic environment caused by the harmful event, such as price erosion.18 For a business, the main elements of the economic environment that may be affected by the harmful event include the prices charged by rivals, the demand facing the seller, and the prices of inputs. For example, misappropriation of intellectual property may cause lower prices because products produced with the misappropriated intellectual property compete with products sold by the owner of the intellectual property.19

In contrast, some types of harmful events do not change the plaintiff’s economic environment. The theft of a small amount of the plaintiff’s products would not change the market price of those products, nor would an injury to a worker change the general level of wages in the labor market. A damages study need not analyze changes in broader markets when the harmful act plainly has minuscule effects in those markets.

In situations where the plaintiff claims price erosion, the plaintiff may assert that absent the defendant’s wrongdoing, a higher price could have been charged and therefore that the defendant’s harmful act has eroded the market price. The defendant may reply that the higher price would lower the quantity sold. The parties may then dispute how much the quantity would fall as a result of higher prices.

Example: Valve Maker infringes Rival’s patent. Rival calculates lost profits as the profits Rival would have made, including a price-erosion effect. The amount of price erosion is the difference between the higher price that Rival would have been able to charge absent

18. See, e.g., Beijing Choice Elec. Tech. Co. v. Contec Med. Sys. USA Inc., No. 18 C 0825, 2020 WL 1701861, at *9 (N.D. Ill. Apr. 8, 2020) (“To prove lost profits damages, a patentee must reconstruct the market that ‘would have developed absent the infringing product,’ and the alleged infringer’s market share may be a relevant data point in this reconstruction. For instance, if an alleged infringer’s market share increases after it introduces the product accused of infringement, that may shed light on what the patentee’s market share would have been had there been no infringement. Or, if an alleged infringer’s market share does not change significantly after it introduces the accused product, that may indicate that lost profits damages are not appropriate because consumers do not care whether the product uses the patented features at issue” (citations omitted)).

19. See, e.g., Power Integrations, Inc. v. Fairchild Semiconductor Int’l, Inc., 711 F.3d 1348, 1382–83 (Fed. Cir. 2013) (“Lost revenue caused by a reduction in the market price of a patented good due to infringement is a legitimate element of compensatory damages. Indeed, an infringer’s activities do more than divert sales to the infringer. They also depress the price [of the patented product].”).

Valve Maker’s presence in the market and the actual price. The price-erosion effect is that price difference multiplied by the combined sales volume of Valve Maker and Rival. Defendant Valve Maker counters that the volume would have been lower had the price been higher, and measures damages using the lower volume.

In more complicated situations, the damages analysis may need to focus on how an entire industry would be affected by the absence of the defendant’s wrongdoing. For example, one federal appeals court held that a damages analysis for exclusionary conduct must consider that absent the defendant’s conduct, firms other than the plaintiff may have entered the market. Competition from such firms would have reduced prices, and as a result the plaintiff’s profits would have been lower than those posited in the plaintiff’s damages analysis.20

Example: Printer Maker has used unlawful means to exclude rival suppliers of computer printer ink cartridges. Rival calculates damages on the assumption that they would have been the only additional seller in the market absent the exclusionary conduct and that Rival would have been able to sell its cartridges at the same price actually charged by Printer Maker. Printer Maker counters that other sellers would have entered the market and driven the price down, and so Rival has overstated their damages.

Comment: Increased competition lowers prices in all but the most unusual situations. Again, determination of the number of entrants that may have been attracted to the market absent the exclusionary conduct, and analysis of their effect on prices, requires a full economic analysis of the industry.

A clear statement of the plaintiff’s situation but for the harmful event is helpful in avoiding double counting that can arise if a damages study confuses or combines reliance and expectation damages.

Example: Marketer is the victim of defective products made by Manufacturer; Marketer’s business fails as a result. Marketer’s damages

20. See Cave Consulting Grp., Inc. v. OptumInsight, Inc., No. 15-cv-03424-JCS, 2020 WL 127612, at *7 (N.D. Cal. Jan. 10, 2020) (no evidence provided that would provide the jury with any basis to disentangle “favorable aspects of an anticompetitive market such as an unnatural price differential between [plaintiff] and [its] competitors and limited competition from third parties because of the difficulty of entering the market.”). See also Sun Microsystems Inc. v. Hynix Semiconductor Inc., 608 F. Supp. 2d 1166 (N.D. Cal. 2009) (holding that a before-and-after damages analysis requires “some showing that the market conditions in the two periods were similar but for the impact of the violation”); Dolphin Tours, Inc. v. Pacifico Creative Serv., Inc., 773 F.2d 1506, 1512 (9th Cir. 1985).

study adds together the out-of-pocket costs of creating the business and the projected profits of the business had there been no defects. Manufacturer’s damages study measures the difference between the profits Marketer would have made absent the defects and the profits Marketer actually made.

Comment: Marketer has mistakenly added together damages from the reliance and expectation measures of damages. Under the reliance measure, Marketer is entitled to be put back to where they would have been had they not started the business in the first place. Damages would be total outlays less the revenues actually received. Under the expectation measure, Marketer is entitled to the extra profits they would have received had there been no product defects. Out-of-pocket expenses of starting the business would have no effect on expectation damages because they would be present in both the actual and but-for worlds and thus would offset each other.

Valuation Issues in the Analysis of Economic Damages

As discussed in the previous section, the analysis of economic damages compares a plaintiff’s economic position in the but-for world—that is, absent any past and future effects of the alleged harmful act on the plaintiff’s economic position—to that plaintiff’s economic position in the actual world, and quantifies the economic value of that difference as of a specific date (the valuation date).21 Because an analysis of economic damages is, by definition, a valuation exercise, it typically requires that economic experts resolve issues arising from the application of valuation approaches to specific case circumstances. This section introduces valuation issues often addressed by economic experts.22

21. As noted in the section titled “The Standard General Approach to Quantification of Economic Damages” above, in some situations the damages analysis aims to quantify the defendant’s gain instead of the plaintiff’s loss. In those situations, the relevant comparison is between the defendant’s economic position in the actual world and the defendant’s economic position in the but-for world—i.e., absent any past and future effects of the alleged harmful act on the defendant’s economic position. The economic issues raised in this section similarly apply when analyzing the defendant’s gain from the alleged harmful act.

22. In the section titled “Damages Issues in Selected Types of Cases” below, we introduce the analysis of economic damages in various case types, namely, consumer product liability, securities, antitrust, and loss of personal income. There, we do not specifically address business valuation disputes. However, the methodologies discussed in this section are also relevant to the analysis of economic damages in the context of business valuation disputes.

Issues Arising When the Potential Impact of the Alleged Harmful Act Is Analyzed Directly on a Particular Date

Issues Arising in Connection with the Use of the Market Price of the Product or Asset at Issue

Because a market price is simultaneously a price that the buying party was willing to pay at the time of the transaction and a price that the selling party was then willing to receive in exchange for the asset or product at issue, a market price provides an objective measure of economic value as of a particular point in time. However, as discussed below, the economic value represented by a market price reflects the specific circumstances under which the transaction occurred. Thus, there is often disagreement among experts as to whether and how the market price of the product or asset at issue can be used to analyze damages. This section summarizes some of the key issues that can generate disagreement.

The market price of the product or asset at issue in litigation is a frequent input to the analysis of damages on a particular date. A simple example of such a situation would be where the defendant’s negligence caused total destruction of the plaintiff’s cargo of wheat, worth $17 million at the then-current market price of wheat. In this simple example, a damages expert may calculate damages as just that amount, $17 million.

Market prices are often used to analyze the plaintiff’s economic position in the but-for world, the actual world, or both. For example,

- In the simple example above, involving a destroyed cargo of wheat, the market price of wheat at the time of the defendant’s negligence may be used to value the plaintiff’s economic position but for the alleged harmful act (i.e., the $17 million value of the plaintiff’s cargo of wheat had it not been destroyed).

- In a consumer fraud case involving a product falsely represented to have certain desirable characteristics, the market price of the product may be used to measure the plaintiff’s actual economic position at the time of purchase (i.e., how much the plaintiff paid for the product).

- In a defamation case involving a publicly traded company plaintiff, the change in the company’s stock price around the time of the defendant’s defamatory act may serve as an initial input to the analysis of the difference in the plaintiff’s economic position between the but-for world (e.g., using the stock price shortly before the defamatory act) and the actual world (e.g., using the stock price shortly after the defamatory act).

However, disagreement often arises among experts as to whether market prices (or changes in market prices over certain periods) serve as an adequate input to analyzing the impact of the alleged harmful act on the plaintiff’s economic position.

First, when using market prices to value the plaintiff’s economic position in the but-for world, disagreements may arise as to whether (and, if so, by how much) the market price that the expert relied on for their analysis represents a value that was itself impacted by the alleged harmful act. If the value represented by the market price reflects the impact of the alleged harmful act, such impact must be removed from the market price in order to properly value the plaintiff’s economic position in the but-for world.

For example, if the destroyed cargo of wheat mentioned above was large enough that its destruction significantly constrained the supply of wheat, thereby increasing the market price of wheat, then the market price of wheat immediately following the destruction of the cargo of wheat will overstate the plaintiff’s economic position but for the alleged harmful act and, thus, will overstate damages. In that case, disagreement may arise among the experts as to the extent to which the market price of wheat was affected by the defendant’s negligence. Moreover, disagreement may arise with respect to what statistical or economic methodologies should be used to quantify the necessary adjustment to the market price in order to account for that impact.

Second, when market prices are used to analyze the plaintiff’s economic position in the actual world, disputes may arise as to whether (and, if so, by how much) the market price fully reflects the impact of the alleged harmful act. If the market price does not fully reflect the impact of the alleged harmful act, then it needs to be adjusted using a reliable methodology to properly value the plaintiff’s economic position in the actual world.

For example, suppose that a manufacturer of wood windows with publicly traded common stock treats its windows with a defective preservative, causing the windows to rot. The window manufacturer sues the preservative manufacturer for damages from lost sales and from the cost of replacing the defective windows. The window manufacturer’s expert may be tempted to use the window manufacturer’s stock price following the disclosure of the alleged harmful act as a measure of the manufacturer’s economic position in the actual world. A potential problem with using the market price of the plaintiff’s stock after the alleged harmful act is that the stock market may anticipate recovery in the form of a damages award, and this will attenuate at least some of the decline in price following the alleged harmful act.23 In the extreme, if stock traders expect that

23. Note that this understatement of damages arises when the publicly traded company stands to recover a damages award as the plaintiff in a matter. However, changes in the market price of company stock have a different role in situations, such as a securities matter, where the public company is the defendant. Damages may be overstated by an unknown amount if the release of

the plaintiff will receive exactly full compensation, the plaintiff’s market value is unlikely to change at all when knowledge of the wrongdoing—including the fact that a damages award will be made—hits the stock market. Thus, in this example, the use of the observed market price of the plaintiff company’s stock at the time of the injury understates the actual amount of harm by an unknown amount, so the expert should consider using additional valuation techniques. Disputes may arise among the experts as to which valuation techniques should be used to quantify the harm and how they should be applied.

Third, when market prices are used to analyze the plaintiff’s economic position, disputes may arise as to whether (and, if so, by how much) market prices reflect not just the impact of the alleged harmful act, but also the impact of other factors. Any impact of factors other than the alleged harmful act must be removed from the estimate of economic damages in order to isolate the harm caused by the alleged harmful act.

For example, consider a securities fraud matter where a mining company defendant is alleged to have overstated the size of its mineral reserves and where the company’s stock price declined by 30% following its revelation of the true size of the mineral reserves. Suppose that, on the day the company revealed the true size of its reserves, it also announced that a natural disaster had caused its largest mine to collapse. To quantify the losses, if any, caused by the market learning of the company’s true mineral reserves, it is necessary to disaggregate the impact of that disclosure from the impact of the disclosure of the mine collapse. A dispute may arise as to how the change in stock price should be adjusted to remove the impact of the disclosure of the mine collapse and isolate the impact of the disclosure of the company’s true reserves.

Issues Arising in Connection with the Use of the Market Price of Ostensibly Similar Products or Assets

In many cases, experts cannot take the market price of the product or asset at issue and apply it directly to analyze the plaintiff’s economic position in the but-for world or in the actual world. For example, there may not be a market for the product or asset at issue from which to obtain a market price (e.g., a company may not be publicly traded). However, experts may still be able to use the market prices of ostensibly similar products or assets—often labeled comparables—to analyze the economic value of the product or asset at issue.

previously fraudulently concealed adverse information causes a reduction in the value of the company both because of the adverse information and because the market anticipates that the company will pay a large damages award to investors who overpaid for their shares during the period when the information was concealed.

Identifying products or assets that are ostensibly similar to the allegedly affected product or asset

A common area of disagreement when relying on the market price of comparables to analyze damages is whether the identified comparables are economically similar to the allegedly affected product or asset. For example, in matters involving real estate, experts often identify comparables from the universe of nearby properties with similar characteristics (e.g., property size, condition, proximity to amenities, zoning restrictions). If the identified comparables are not similar to the product or asset at issue along economically relevant dimensions, the comparables’ market prices may not serve as a reliable measure of the economic value of the allegedly affected product or asset (in the but-for world or in the actual world) and may lead the economic expert to significantly misestimate economic damages.

There may also be a dispute as to whether the period when the identified comparables were traded (and thus when their market price was determined) is too distant from the damages valuation date. Temporal distance between the damages valuation date and the period when the selected comparables were traded may cause the market prices of the selected comparables to reflect macroeconomic and business conditions that are significantly different from those in place as of the damages valuation date. In that case, the market prices of the comparable products or assets may not reliably measure the economic value of the product or asset at issue. For example, in a matter involving a sale of a private oil company that took place at a time when oil prices were at historic lows, evaluating the fairness of the sale price by comparing it to the prices at which similar companies were sold during an earlier period (when oil prices were significantly higher) could lead the expert to overstate the value of the company as of the sale date.

Adjusting the market price of ostensibly similar products or assets

Even when experts agree on a list of comparables to use in the damages analysis, disputes may arise as to whether (and, if so, how) the value of the allegedly affected product or asset implied by the comparables’ market prices needs to be further adjusted to adequately measure the economic value of the product or asset at issue.

Accounting for differences between the ostensibly similar products or assets and the allegedly affected product or asset.

Despite experts’ best efforts, circumstances are often such that the best available comparables remain different from the product or asset at issue in economically significant ways. In such circumstances, additional adjustments to account for those differences may

be required to ensure that the economic value of the allegedly affected product or asset is not misestimated. For example, in a matter involving a business valuation, the business at issue may be much smaller than any of the identified comparable businesses, rendering value comparisons inappropriate. Therefore, an expert may propose to restate the value of comparable businesses using valuation ratios—a ratio of some measure of value, such as stock price, to some measure of economic output, such as earnings—and multiply the comparables’ valuation ratios by the measure of economic output for the smaller business to estimate its value, thereby adjusting for size.

However, disputes often arise over whether any adjustments made to the value of the comparables appropriately capture all significant economic differences between the comparables and the product or asset at issue. In the business valuation example, a dispute may arise as to whether the adjustment based on valuation ratios fully accounts for differences between the company at issue and the comparable companies, such as differences in profitability, growth prospects, or riskiness.

Example: Oil Company deprives Gas Station Operator of the benefits of Operator’s business. Oil Company’s damages study starts by calculating the ratio of gas station sale value to gasoline sales for five nearby gas station businesses that have sold recently. The average ratio is $0.26 per gallon of sales per year. The Operator sells 1.6 million gallons per year, so the business was worth $0.26 × 1,600,000 = $416,000, according to the Oil Company’s expert. The expert for the Operator argues that the sales used by the Oil Company occurred before a major business relocated nearby. Thus, the gas station sale value to gasoline sales should be increased to $0.30 to reflect the new growth rate as a result of the expected increase in business. The Operator’s expert calculates the business to be worth $0.30 × 1,600,000 = $480,000.

Accounting for the impact of the harmful act.

In some cases where experts rely on comparables to analyze damages, the alleged harmful act did not cause a total loss of the value of the product or asset at issue, but rather caused only a reduction in its value. In those cases, damages experts may adapt the valuation implied by the comparables to measure the loss caused by the alleged harmful act—that is, the difference between the plaintiff’s economic position in the but-for world and in the actual world. For example, in a business valuation case, an expert may propose to use valuation ratios to analyze damages, as illustrated by the numerical example below, although disputes may arise as to their appropriateness.

Example: Oil Company breaches an earlier agreement with Gas Station Operator and opens another station near Operator’s station. As a result, Operator’s gasoline sales are reduced by 700,000 gallons per year. Oil Company’s damages study applies an average valuation ratio (based on recent sales of gas station businesses) of $0.26 per gallon of sales per year to the reduction in sales: $0.26 × 700,000 = $182,000. In contrast, Operator’s damages study uses a statistical analysis (also based on recent sales of gas station businesses) that finds the impact of sales on gas station value depends on the total sales volume of the gas station, such that, given the Operator’s level of sales absent the breach, each additional (or marginal) gallon of subtracted sales reduces value by $0.47. As a result, the Operator’s expert calculates damages of $0.47 × 700,000 = $329,000.

Comment: Because fixed costs associated with running a gas station (e.g., rent) are diluted by larger sales amounts, the average valuation of gasoline sales will be less than the marginal valuation. Thus, a damages model that accounts for the level of sales absent the breach is the conceptually correct approach.

Issues Arising in Connection with the Use of Models to Simulate the But-For Price

In certain cases, experts cannot adjust the market price of the asset or product at issue—or of ostensibly similar assets or products—to reflect the impact of the alleged harmful act. In these cases, some experts have used statistical and economic models to simulate market prices in the but-for world.

It is well established in economics that market prices are determined by supply and demand. To estimate market prices in the but-for world, experts have proposed models that seek to represent the price-formation process, or the outcome of that process, in the relevant market when supply and demand for the asset or product at issue exclude the effects of the alleged wrongdoing. Experts rely on assumptions that simplify some of the complexities of real markets and focus their analysis on the specific impact of the harmful act.

Experts also rely on a wide variety of data to estimate the relevant variables and parameters of their models and represent real markets to a reasonable degree of accuracy. These data can include market data such as prices and quantities sold of the asset or product at issue, or the prices and quantities sold of related assets or products (such as substitute and complementary products). Experts can also rely on nonmarket data, such as accounting data or data generated via surveys.

Disagreements occur with respect to the assumptions and data used in these models. This section summarizes certain issues that arise when experts rely on statistical and economic models to simulate or approximate but-for prices.

Realistic modeling of preferences, incentives, and constraints of buyers and sellers

Experts use economic and statistical models to simulate real markets or market outcomes by focusing on the analysis of certain key elements and relationships of the market and by making assumptions about the influence of other less relevant characteristics. For a model to be useful, it needs to provide a sufficiently realistic representation of the relevant market. This usually involves defining the key characteristics of supply and demand of the asset or product at issue. Disputes may arise over which assumptions about demand and supply more realistically reflect the relevant market in the but-for world.

A valid model must provide a sufficiently realistic representation of the preferences of buyers. Experts usually achieve this by relying on methods of demand estimation commonly used by economists and marketing academics. These methods are broadly classified in two categories. The first category, known as the revealed preference method, relies on data from the choices made and prices paid by buyers in the real world to infer the underlying preferences and restrictions of buyers. The second category, known as the stated preference method, relies on data from surveys of relevant subjects that are considered representative of the population of buyers of the asset or product at issue.

When data from surveys are used, disputes may arise about whether such data accurately represent respondents’ preferences—respondents may behave differently when taking a survey compared to how they would behave in the real market. Disputes may arise about how realistically a survey represents the environment in which buyers make purchase decisions in the real world, or about how accurately the sample of survey respondents represents the relevant population of buyers. Refer to the Reference Guide on Survey Research, in this manual, for a detailed treatment of these and other issues that arise when surveys are conducted.

A common question that arises when experts rely on a model to represent demand for an asset or product is whether the model appropriately accounts for variation in the preferences of different groups or types of buyers. For example, in an intellectual property dispute, an expert could use an economic model to estimate the price of a brand-name drug covered by a patent in a but-for world where the patent was not enforceable and generic drug manufacturers were allowed to compete. An overly simplistic model of demand could lead to a prediction that the entry of generic drug manufacturers into the market would result in a decrease in the price of the brand-name drug. However, a more realistic demand model

that takes into account the preferences of different types of consumers could lead to a finding that the market price of the brand-name drug would increase as the smaller segment of consumers who are brand-conscious would be willing to pay more for the brand-name drug.

A valid model must also provide a sufficiently realistic representation of the preferences and incentives of sellers. In many cases, experts rely on simplifying assumptions to represent the characteristics of supply. Some experts have assumed that the supply quantity is fixed at the quantity that was sold in the actual world. Other experts rely on economic frameworks to account for the changes in the economic position of sellers. These frameworks may include simplifying assumptions about the general relationship between the quantity offered and the price offered in the market or may include sophisticated models that simulate the behavior of individual sellers. Disputes commonly arise about whether the assumptions made by an expert regarding supply reflect the true positions and incentives of the suppliers in the but-for world.

Defining a valid model of supply generally requires consideration of key characteristics of the market that may influence the prices that consumers pay. For example, in a dispute involving the alleged mislabeling of a prescription drug’s potential side effects, an expert must consider that the prices that consumers pay for prescription drugs may be influenced by insurance companies that can negotiate prices with the manufacturer and that can adjust consumer prices based on copays and deductibles.

It may also be necessary to define the characteristics of key competitors, distributors, retailers, and other relevant market participants. For example, a model that attempts to measure the impact on ticket prices of an alleged anticompetitive agreement between two bus lines should take into account available alternative means of transportation, such as cars, trains, or possibly airplanes. Disputes may arise as to the number, type, and characteristics of relevant alternatives consumers may have.

Modeling the impact of the alleged misconduct on demand and supply

To be helpful in the estimation of damages, a model of but-for prices must adequately reflect supply and demand absent the alleged misconduct while excluding the influence of unrelated factors. In general, the more complex the allegations are, or the more complex the facts surrounding the allegations are, the more difficult it will be for an economic model to reliably estimate market conditions absent the alleged misconduct.

Complex allegations may require more flexible models to represent the but-for world adequately. In general, models that allow more flexibility and that

provide the expert with more control over how to represent demand and supply in the but-for world are more difficult to estimate, and require larger amounts of data. For example, consider a dispute between a large buyer of insurance and an insurance company in which the allegations involve whether the insurer properly invoked a complex set of conditions to cancel a portfolio of policies and avoid paying for them. The damages model would require significant flexibility to perform the valuation of the portfolio in a but-for world where the defendant insurer could invoke some, but not all, of the cancellation conditions that it did in the actual world. Disputes commonly arise about whether an expert model adequately reflects complex allegations.

A model used by an expert should be able to account for the impact of confounding factors unrelated to the allegations but that may result in the same type of harm alleged. For example, in a dispute about potential contamination of groundwater from an industrial plant, an expert could estimate a statistical model—known as a hedonic model—to predict home prices based on certain characteristics of a home (e.g., number of bedrooms, number of bathrooms, etc.). The expert could attempt to use sale price data of homes before and after the alleged contamination event to estimate the impact of the alleged contamination on home values. However, if a zoning change affecting the properties at issue was enacted around the same time as the alleged contamination event, the expert’s model would need to distinguish any decrease in the price of homes from the alleged contamination from any decrease (or increase) due to the zoning change. Disputes commonly arise about whether an expert model adequately controls for the impact of confounding factors.

Surveys provide the expert with some control over how to represent the but-for world via the information conveyed to survey respondents. However, disputes may arise about the specific information that respondents are assumed to have in the but-for world. For example, an expert could propose a survey to analyze how consumers would react to a label disclosing the use of genetically modified corn on a package of cereal labeled “100% natural corn.” Experts may disagree about the wording, size, and placement of such a label, all of which can affect the damages estimate arising from the survey.

Accounting for Market Frictions

When relying on market data to analyze economic damages as of a specific date, it may be necessary to consider how market frictions may have impacted market prices—whether it be the price of the allegedly affected product or asset or the price of ostensibly similar products or assets.

Perfectly competitive markets have what economists term a frictionless market structure. These markets have (1) a large number of buyers and sellers

of a single, homogeneous product; (2) fully informed participants; and (3) the feature that participants can easily enter or exit from the market. A friction is anything that prevents the market from being perfectly competitive. Economists have identified various types of market frictions that can impact market outcomes, including market power (e.g., oligopolies), adverse selection, and taxes.24

For example, markets for businesses and properties have frictions that may make transaction values depart from the usual concept of the price negotiated by a willing seller and a willing buyer. In the case of a forced sale, and thus a less willing seller, the transaction price may understate the value. Adverse selection, which occurs when one party knows more about a property or business than the other, may cause severe failures in some markets.25 Sales prices tend to be lower when equipment with hidden defects cannot be distinguished from equipment in unusually good condition. This is because buyers are only willing to pay a lower price that reflects the possibility of hidden defects in the equipment and because owners of equipment in good condition may choose not to offer it at that lower price.

Example: Negligence of Tire Maker causes the total loss of a Boeing 737 airplane. Tire Maker’s damages analysis uses the prices of 737s of similar age in the used airplane market to set a value of $23 million on the ruined airplane. However, Airline offers the testimony of an economist expert who explains that only a small fraction of 737s are ever put up for sale in the used airplane market. Rather, airlines choose to sell only defective airplanes because they continue to fly nondefective 737s. The expert then adjusts for the adverse selection of inferior airplanes in the used airplane market and places a value of $42 million on the airplane.

Comment: Airline expert’s adjustment is merited in principle, although it is challenging to carry out and is likely to be the subject of expert disagreement.

In financial markets, differences in information available to different market participants or limited asset liquidity can lead to market prices that differ, sometimes significantly so, from the prices that would have prevailed in perfectly competitive financial markets. For example, the sale of a large block of shares of

24. A comprehensive treatment of economic frictions is outside the scope of this reference guide.

25. See, e.g., George A. Akerlof, The Market for “Lemons”: Quality Uncertainty and the Market Mechanism, 84 Q. J. Econ. 488 (1970), https://doi.org/10.2307/1879431.

a company’s common stock may happen at a price that is much lower than recently prevailing market prices because potential purchasers of that block of shares are concerned that the seller might have negative, material nonpublic information about the value of the shares.

A major source of friction in property and business markets is the capital gains tax. Because capital gains are taxed only at realization, subtracting the amount of unrealized capital gains taxes from the value of a business or property would generally understate the value of the business or property to the existing owners if they have no plans to sell, except in the very distant future.

Issues Arising in Connection with the Use of Repair or Abatement Costs

In some cases, economic damages can be calculated as the costs that the plaintiffs incurred or would incur to restore their economic position from the actual world to the but-for world in which the alleged harmful act did not occur. These costs could include repair costs (e.g., the cost of the parts and labor used to repair a defective product), replacement costs (e.g., the cost of a third party hired to perform a task that the defendant was contracted to do but did not), or the costs of reducing or abating any harm caused by the alleged misconduct (e.g., the cleanup costs following an environmental contamination incident).

Damages experts often disagree on how to calculate these costs. First, experts may disagree on whether any costs allegedly incurred are attributable to the alleged misconduct. For example, if a service hired by the plaintiff to repair an allegedly defective product also performed general maintenance, the total cost paid may overestimate damages. Second, experts may disagree on the costs that are necessary to repair or abate the consequences of the alleged misconduct. For example, in a case where the plaintiff alleges that they will need to install expensive air filtration devices to reduce foul odors from a defective air conditioning system, experts may disagree on whether such costs are necessary if cheaper alternatives (e.g., more frequent maintenance) are available. Third, experts may disagree about whether the potential costs of repair match the economic value of the loss experienced by the plaintiff. For example, consider a builder who in the process of selling a house learned that a contractor used cheaper materials than promised. Assume that the cost of removing the cheaper materials and replacing them with the materials originally specified would be $100,000; however, the builder was able to sell the home by offering a discount of only $50,000. In this case, the replacement costs would overstate the economic loss suffered by the builder.

Issues Arising When the Potential Impact of the Alleged Harmful Act Spans Multiple Dates and Damages Are Analyzed Indirectly on a Single Date

Having discussed various issues that arise when experts analyze damages by assessing the impact of the alleged harmful act on a specific date directly, we now turn to issues arising in situations where economic experts analyze damages on a particular date indirectly. Specifically, we turn to situations where experts first assess the direct economic impact of the alleged harmful act (i.e., the flow of economic income or loss at a specific point in time that can be causally linked to the defendant’s alleged misconduct) over multiple dates (e.g., the lost profits from operating a facility that was expected to produce widgets for a long period of time but was destroyed by a defendant’s misconduct) and then value the cumulative direct impact over multiple dates as of a single valuation date.

Estimating the Period-by-Period Direct Impact of the Alleged Harmful Act

In situations where experts assess the direct economic impact of the alleged harmful act over multiple dates, it is necessary to estimate flows of economic income or loss to the plaintiff in past and future periods that resulted (or were expected to result) from the alleged harmful act. In doing so, experts face a number of considerations.

Many of those considerations, such as how the actions of plaintiffs and defendants would have differed had the alleged harmful act not occurred, or whether all economic consequences of the alleged harmful act have been considered, have been introduced more broadly in the section titled “Valuation Issues in the Analysis of Economic Damages” above. This section further explores these considerations in the specific context of assessing the period-by-period direct economic impact of the alleged harmful act.

Disputes about how the defendant’s actions would have differed had the alleged harmful act not occurred

When analyzing damages, experts often rely on the plaintiff’s allegations (e.g., as stated in a complaint or statement of claim) as the basis for identifying the alternative actions that the plaintiff alleges the defendant should have undertaken instead of the alleged harmful act. However, in some cases, the plaintiff’s

allegations do not specify fully what the defendant could and should have done instead of the alleged harmful act, or the allegations are squarely contradicted by case facts. For example, consider a derivative lawsuit where a company’s shareholders sue the CEO for using the firm’s funds in wasteful company acquisitions that are expected to reduce the company’s quarterly profits for periods lasting well into the future. The plaintiff’s allegations may leave unspecified what the CEO should have done with the funds instead of the allegedly wasteful acquisitions or the allegations may assume that certain investment opportunities were available that the record demonstrates were not.

Depending on the circumstances, the ambiguity remaining in the allegations may be significant enough that it causes experts on opposite sides of the litigation to reach substantially different estimates of damages. For example, in the case of the CEO alleged to have engaged in wasteful corporate acquisitions, the expert retained by the CEO defendant may assume that the funds used to finance the acquisitions would have been used to fund internal projects that were expected to be as unprofitable as the wasteful acquisitions. On the other hand, the expert retained by the investor plaintiffs may assume that the funds would have been distributed to the shareholders as quarterly dividends instead. Thus, when assessing opposing experts’ damages analyses, a critical issue may be how each expert modeled what the defendant’s actions would have been had the alleged harmful act not occurred.

When the plaintiff’s allegations are consistent with any of several alternative actions that the defendant might have taken had the alleged harmful act not occurred, there is a risk that expert analyses become tainted by hindsight. With the benefit of hindsight—often, after years have passed since the alleged harmful act occurred—the parties may instruct their experts to assume that the defendant would have taken particular actions (among various possible alternatives that are consistent with the plaintiff’s allegations) that lead to a more favorable damages number. However, the defendant’s actions, had the alleged harmful act not occurred, would have been based on the defendant’s knowledge at the time of the alleged harmful act, and not on whatever knowledge only later became available, including as a result of litigation. In the example above involving wasteful corporate acquisitions, depending on what the CEO contemporaneously knew, had the alleged harmful act not occurred, the CEO’s decision could have been either to pay out the funds as dividends (as the shareholders’ expert assumed) or to reinvest the funds into internal projects (as the CEO’s expert assumed).

Disputes about how the plaintiff’s actions would have differed had the alleged harmful act not occurred

Even when a defendant’s actions, had the alleged harmful act not occurred, are fully specified, there may be disagreements about what the plaintiff would have done in the hypothetical world where the alleged harmful act did not occur. Such

disagreements may also lead to significantly different damages numbers. Take the numerical example below, where the plaintiff in a real estate matter argued that undeveloped land was taken from him by the defendant’s harmful act and that damages should include the value of the undeveloped land, as well as the value of the stream of monthly rental income for years to come that the plaintiff would have earned had the plaintiff been able to develop the land.

Example: Property Owner sues County for the value of undeveloped property condemned for a rapid-transit extension. Property Owner’s damages claim is $18 million, which is the appraisal value of a hypothetical condominium development on the property less the anticipated cost of building the development. The County’s expert, an appraiser, argues that the market value of the property is $2 million, based on comparable undeveloped land nearby.

Comment: In principle, if the real estate market is perfectly competitive, the current market value of undeveloped land and the market value of the same land with proper development, less the cost of that development, should be the same, because buyers would bid for the developed properties based on the value of the undeveloped land. Thus, Property Owner may have understated the development costs. But the value of nearby properties used as comparables may understate the value of the condemned property—they may be available for sale because they lack certain features that would make them more desirable to develop, such as a view. On the other hand, the Property Owner’s valuation does not reflect the probability that the Property Owner may not succeed in building the condominium.

Moreover, as was the case with respect to modeling the defendant’s actions had the alleged harmful act not occurred, there is a risk that expert analyses may be tainted by hindsight when making assumptions about what actions the plaintiff would have taken, had the alleged harmful act not occurred.

Disputes about whether all economic consequences of the alleged harmful act are being accounted for

Another area where disputes may arise when analyzing the direct economic impact of the alleged harmful act over multiple periods is whether the experts’ damages analyses have fully considered all the reasonably foreseeable economic consequences of the alleged harmful act. Failure to fully consider all reasonably foreseeable economic consequences of the alleged harmful act may lead experts to estimate damages incorrectly, possibly significantly so.

For example, where the injury takes the form of lost sales volume, the plaintiff usually has avoided the cost of production for the lost sales. Thus, an expert would overstate damages by not including the avoided costs of production as a reduction in the estimated direct economic impact of the alleged harmful act. Calculation of these avoided costs is a common area of disagreement about damages. Conceptually, avoided cost is the difference between the cost that would have been incurred at the higher volume of sales but for the alleged harmful act and the cost actually incurred at the lower volume of sales achieved. The avoided-cost calculation is done for each period. The following are some of the issues that arise in calculating avoided cost:

- For a firm operating at capacity, expansion of sales is cheaper in the longer run than in the short run; however, if there is unused capacity, expansion of sales may be cheaper in the short run.

- The costs that can be avoided if sales fall abruptly are less in the short run than in the longer run.

- Avoided costs may include marketing, selling, and administrative costs as well as the cost of manufacturing.

- Some costs are fixed, at least in the shorter run, and are not avoided as a result of the reduced volume of sales caused by the harmful act.